Côte d’Ivoire boasts an impressive network of over 400,000 mobile money service points, a figure that dwarfs the total number of ATMs by 300 times, according to the Agency for the Promotion of Financial Inclusion. Ivorians rely heavily on these convenient kiosks for their daily financial needs, from depositing salaries to withdrawing cash. However, a recurring problem is casting a shadow over this vital service: mobile money agents frequently encounter a scarcity of liquid funds, significantly hindering their operations.

As evening approaches in Abidjan’s bustling Angré Château district, the daily rush for groceries and public transport is in full swing. Yet, at a prominent mobile money booth, a familiar problem unfolds: a severe cash deficit. Rosette, hoping to withdraw 10,000 CFA francs (approximately 15 euros), accepts the situation with resignation. “When you come, they don’t have what you need; it’s just something that happens, so we deal with it,” she explains.

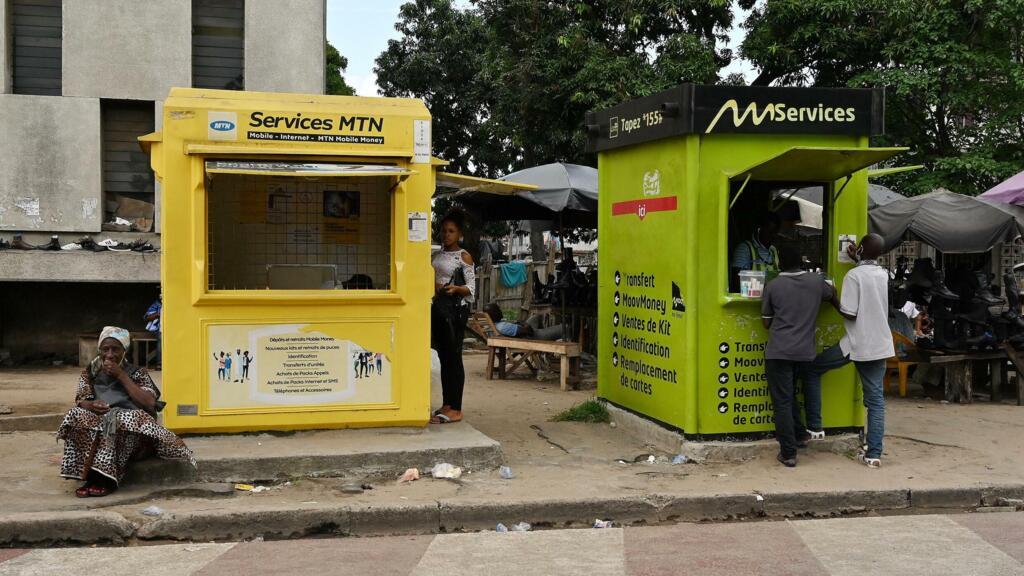

Inside the bright yellow kiosk, teller Nema manages a growing line of customers. “Some days see a lot of withdrawals, and we simply run out of cash. We apologize and inform clients that we’re currently in deposit-only mode,” she states. Faced with long waits, many customers choose to seek services elsewhere.

Affoué, the manager of this particular kiosk and a former accountant, understands the direct impact of losing a customer. “You lose the client, and you lose the client’s commission. That’s why it’s crucial to serve clients well so that commissions can increase and generate a net profit,” she emphasizes.

Client attrition, profitability erosion

Mobile money operators such as Orange, Moov, MTN, and Wave compensate kiosk managers with a commission for each transaction. For instance, agents typically earn between 20 and 60 CFA francs (about 3 to 9 euro cents) for a 10,000 CFA franc transaction. Consequently, higher transaction volumes and values directly translate into increased revenue for these agents.

However, this system grinds to a halt when agents face cash or credit shortages. They are then compelled to temporarily close their operations to resupply funds from operators or banks. This interruption leads to a “loss of clientele, insufficient commissions, and reduced profitability for them. They are forced to close their agencies to visit distributors,” as one agent lamented.

Motorcycle couriers: boosting responsiveness

Recognizing this critical bottleneck, Gertrude Yapi, Operations Director at Leya, an Abidjan-based startup, has pioneered a solution: a motorcycle-based fund transfer service for mobile money points. “We replenish their credit in under four minutes and deliver cash in less than 30 minutes to satisfy customers,” Yapi explains. She asserts that Leya’s service enables points of sale to achieve a 50% increase in turnover. Currently, Leya serves over 3,000 active clients across four key Ivorian cities: Abidjan, Bondoukou, Bouaké, and Korhogo.

From an economic standpoint, Ivorian economist Kassoum Timité stresses the vital importance of continuous service for overall economic activity. “Mobile money directly serves the informal sector, which accounts for the largest share of Côte d’Ivoire’s economic activity—estimated by the International Monetary Fund to contribute up to 40% of the Gross Domestic Product. Therefore, a lack of liquidity will slow down transactions, and economic activity will also decline,” Timité warns.

In 2024, daily mobile money exchanges in Côte d’Ivoire surpassed 140 billion CFA francs (over 210 million euros), a nearly fourfold increase compared to 2020, highlighting the service’s rapid expansion and crucial role in the nation’s financial landscape.