Niger’s Soaring Non-Performing Loans Cast Shadow Over West African Banking Stability

In January 2026, a regional financial outlook report delivered a stark warning: while the banking system of the West African Economic and Monetary Union (WAEMU) reached new symbolic milestones, it is increasingly undermined by a rising tide of credit risks. At the epicenter of this financial turbulence, Niger stands out with an unprecedented non-performing loan (NPL) ratio, signaling a growing divide within the bloc.

Niger’s Deteriorating Loan Portfolio: A Regional Outlier

As the WAEMU struggles to stabilize its financial framework, Niger’s banking sector remains the most fragile in the region. Despite marginal improvements, the country’s loan default rate continues to eclipse all others, reinforcing its reputation as the weakest link in West Africa’s financial chain.

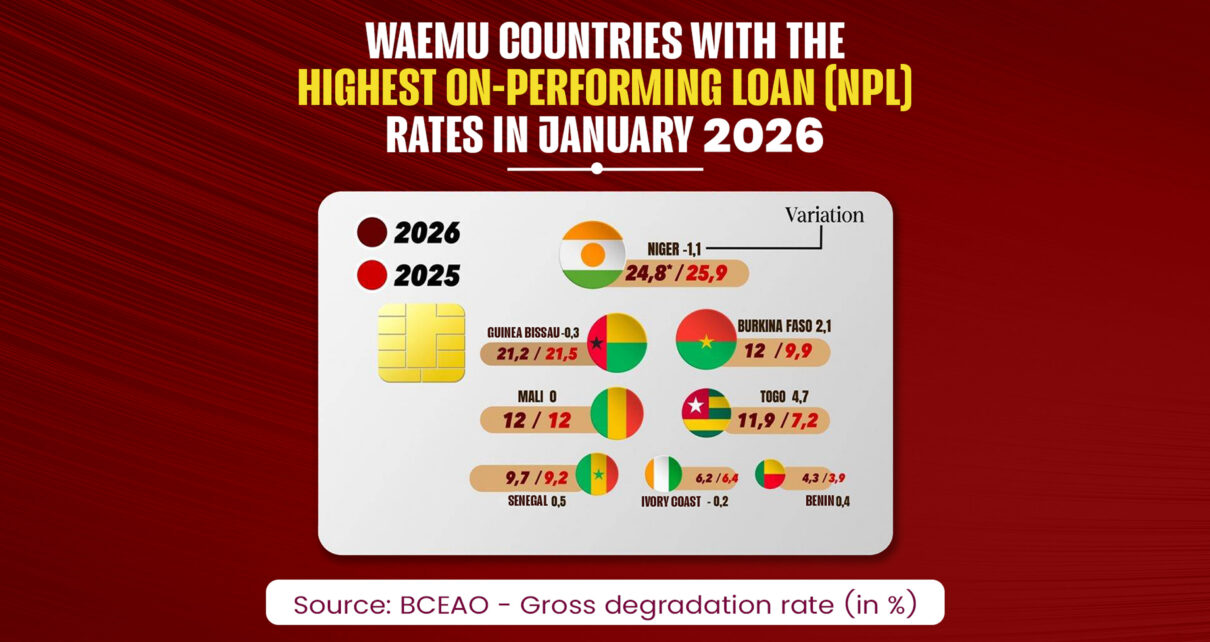

With a 24.8% NPL rate in January 2026, Niger holds the unenviable distinction of leading the regional ranking. Nearly one in four loans granted in Niger is now classified as non-performing—a figure that, although slightly improved from 25.9% in 2025, remains alarmingly high compared to the regional average.

Analysts attribute this vulnerability to structural weaknesses exacerbated by persistent security challenges and political instability. The gap between Niger’s NPL rate and the regional norm underscores an exceptional exposure to systemic risk, raising concerns about the country’s long-term financial resilience.

A Tale of Two Blocs: Coastal Resilience vs. Sahelian Strain

The January 2026 data reveals a sharp divide between the more stable coastal economies and the beleaguered Sahelian bloc, where Niger serves as a crisis focal point.

The Sahelian Bloc: A Region Under Pressure

Beyond Niger, other Sahelian countries are also grappling with elevated NPL rates:

- Mali and Burkina Faso: Both nations report NPL rates of 12%. Burkina Faso’s rate has surged by 2.1 percentage points over the past year, signaling a rapid deterioration in credit quality.

- Guinea-Bissau: The country remains in a critical zone with a 21.2% NPL ratio, second only to Niger.

The Coastal Bloc: Relative Stability with Notable Exceptions

In contrast, coastal WAEMU members demonstrate greater financial resilience, though not without exceptions:

- Benin: Emerges as the region’s top performer with the lowest NPL rate at 4.3%.

- Côte d’Ivoire and Senegal: Both countries maintain stable ratios of 6.2% and 9.7%, respectively.

- Togo: The outlier in this group, with a dramatic spike in NPLs—jumping from 7.2% to 11.9% in a single year (+4.7 percentage points).

The Bigger Picture: Credit Growth Stalled by Rising Defaults

The WAEMU’s total loan portfolio surpassed 40,031 billion CFA francs in January 2026, marking a 4.7% year-on-year increase. Yet this growth is overshadowed by growing concerns over credit quality.

Non-performing loans now total 3,631 billion CFA francs, with the coverage ratio plummeting to 59%. This means banks are struggling to provision for losses at a pace that matches the rise in defaults, signaling potential liquidity strains ahead.

Banks Tighten Lending Standards in Response to Risk

Faced with the deteriorating credit profiles of Sahelian nations—particularly Niger—banks have adopted a more cautious approach:

- Stricter lending criteria: Higher personal contributions and more stringent collateral requirements are now standard.

- Selective credit expansion: Lenders are prioritizing balance sheet safety over lending growth, potentially stifling financing for local SMEs and SMEs.

As the WAEMU’s banking system stands at a crossroads in early 2026, the dual pressures of Niger’s NPL crisis and the broader Sahelian downturn demand heightened vigilance. While the bloc’s overall financial stability remains intact for now, the risk of a liquidity crunch looms large if current trends persist.